Concept

Entity Financing

Jump To

Problem

The abundance of state and federal funding over the past five years has led many agencies and organizations to rely heavily on grant funding for implementing restoration and infrastructure projects.

The Trump administration’s cuts in 2025, combined with California’s periodic surpluses and deficits in state funding, demonstrate the vulnerability of grant funding dependence. Many organizations are familiar with the cyclical nature of funding sources and seek to create more dependable, even-keeled funding streams, although grants can often complement stable revenue streams. Rough estimates for JPA creation in California for 2025 range from a bare bones budget of approximately $400,000 per year, with one region stating that a more “inflation-proof” budget could be as high as $2-3 million/year for startup and sustainable implementation over time.

Resources & Reports

- Funding Options and Strategies for a new Joint Powers Authority

- Tahoe Central Sierra Pilot Project: Funding Options and Strategies for Potential New Joint Powers Authority

- Wood Product Development to Support Non-Industrial Land Management (Legal Report Supplement)

- North Coast Wood Product Development and Economic History Snapshot (Economic report)

- Lake County RRA Financial Analysis Study

- Marin County Chapter 4: Economic Viability and Investment Opportunities (link coming soon)

- Marin County Appendix G – Economic and Pro Forma Financial Analyses (link coming soon)

Solution

Many of the Office of Land Use and Climate Innovation’s CALFRAME feedstock aggregation pilots recognized the need for long-term funding sources and that grants are not a dependable resource to maintain an organization over time. Traditional funding sources are many, and a blended portfolio should help weather changes in grant cycles and tap into funding sources that can provide steady revenue.

In Depth Concept Description

Guest post adapted from Vance Russell’s (3point.xyz) article on JPA Funding Strategies

Traditional sources of funding are described below, with the pluses and minuses of each summarized in (Table 1.1). Other revenue sources, such as climate bond funding, agency funding, and legislative action, are also available, but their outcomes tend to be grant-based and temporary.

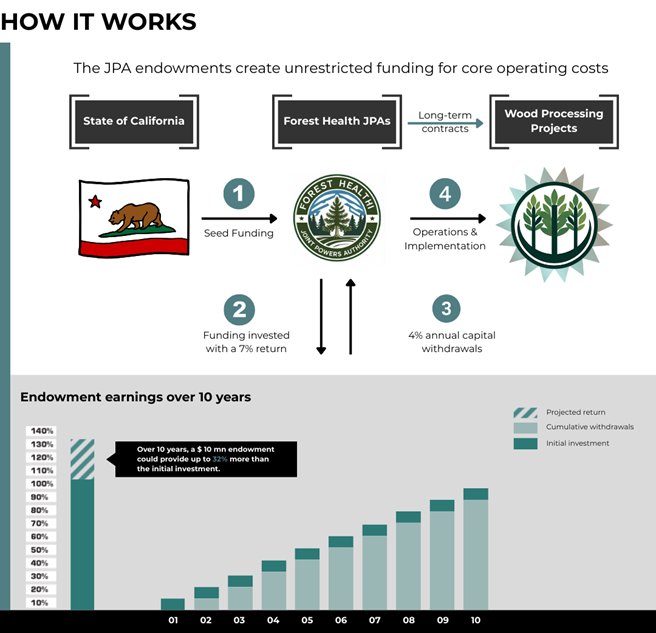

- Endowment. In the case of the feedstock aggregation pilots, the LCI provided a funding tranche to kickstart JPA creation. This funding could potentially be used to create an endowment or, at the very least, seed an endowment that could provide a steady source of unrestricted revenue if invested wisely.

- Contributions. A capital campaign to raise awareness about a JPA and generate individual, corporate, and foundation grants would complement any secured funds. Match from non-public sources often makes grant applications more competitive.

- Federal and State Grants. JPAs should be competitive for a variety of state and federal grants and be able to budget overhead costs (~10%) and directly bill salaries to cover a portion of operating costs.

- Member Contributions. JPA members or beneficiaries, such as RCDs, pay an annual cost to participate in the feedstock aggregation program.

- Fee-for-service. Charging fees for forest management, timber harvest plans, feedstock contracts, or grant administration, depending on the skills of the JPA staff, could be another way to generate a steady income source. Western Shasta RCD, for example, works with non-industrial forest owners to develop forest management plans.

- Sort yards. Managing a sort yard for aggregated feedstock could be a strategic revenue source, but some regions found a lack of feasible revenue for sort yards. Note that feedstock aggregation and sort yards should not be conflated, nor should the creation of JPAs be thought of as sort yard managers. The Northeast pilot found that sort yards are not viable for their region.

Endowment-based funding represents a promising and underutilized strategy for ensuring the long-term financial sustainability of JPAs engaged in forest health and feedstock aggregation. Unlike grant-dependent models, which are vulnerable to the cyclical nature of public budgets and shifting political priorities, endowments can provide a stable and predictable revenue stream. Endowments may be the most strategic way to fund JPAs, especially since some may struggle to secure grant funding in the future, given their long-term focus on feedstock supply contracts.

By investing a substantial principal—such as an initial gift of $10 million—and supplementing it with modest annual contributions, a JPA can generate consistent income to support core operations, staffing, and potentially even programmatic expansion. The administrative burden and ongoing costs associated with managing an endowment are typically lower than those required for continuous grant writing and reporting, making this approach attractive for organizations seeking to minimize overhead.

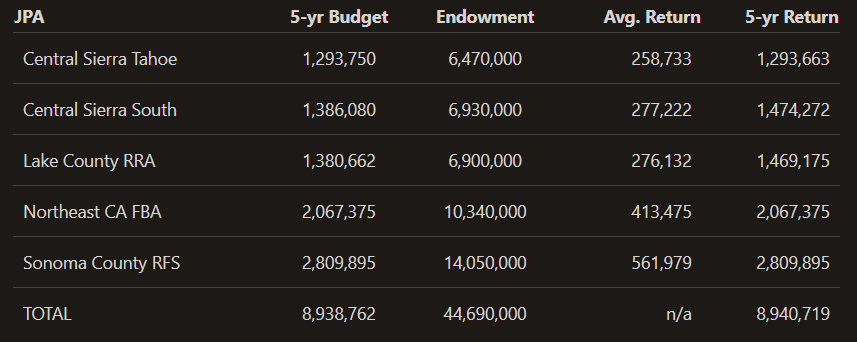

Russell developed an example endowment return schedule based on five pilot JPA annual budget estimates. The 5-year budget is an estimate from the respective JPA proponents. An estimated 0.2% administrative fee and $5,000 contribution to the principal are included in the calculations. The Central Sierra South example is being developed from an existing JPA (Central Sierra Economic Development District or CSEDD) and, therefore, may not be directly comparable to the other four startup JPAs. A similar example in development is the Eastern Sierra Council of Governments (ESCOG). RRA = Risk Reduction Authority, FBA = Forest Biomass Authority, RFS = Regenerative Forest Solutions. JPA endowments are not limited to these examples.

With a conservative yearly return of 7%, a spending rate of 4%, and an administrative fee of 0.2%, an endowment of $10 million could yield approximately $400,000 in its first year, with annual income rising to nearly $448,000 by year 5 (see table below). This steady growth not only insulates a JPA from the volatility of state surpluses and deficits but also frames endowment funding as a long-term cost-avoidance strategy for public agencies and private donors alike.

An innovative approach to multiplying the impact of a JPA’s funding endowment is to allocate a portion of the principal for low-interest loans to forest health operations and wood products businesses. By acting as a community-based lender, the JPA can support local projects that might otherwise struggle to access affordable capital, accelerating restoration and market development. The interest payments received from these loans can then be reinvested into the endowment, steadily growing the principal over time. This strategy not only amplifies the reach of the original endowment but also creates a self-reinforcing cycle of investment and impact, enhancing both financial sustainability and landscape resilience.

The economics of a revolving loan fund depend on several key factors: the total annual return from the principal, the yearly amount loaned out, the interest rate charged, and the loan performance period. If the JPA governing board added guardrails to revolving loan spending, interest rates, and other factors, presumably 1-2% of the return could be set aside for a loan fund that is carefully loaned to local organizations when a predetermined amount is reached. If the loan interest rate is a point or two above the endowment earning rate, then that would allow the revolving loan principal to grow. There’s a risk of unpaid loans, loans that take too long to repay, or excessive loan amounts, but these factors could all be mitigated through the JPA’s bylaws.

Over 10 years, a $10,000,000 endowment with a 7% annual return, 4% annual spending, a 0.2% administrative fee, and $5,000 added each year would generate a steadily growing cumulative loan pool. By setting aside the yearly earnings above the spending and administrative costs, the loan pool would reach approximately $3.2 million by year ten. This approach allows the JPA to support additional projects through low-interest loans while maintaining the long-term growth and stability of the endowment.

Any funding strategies, whether they are traditional or new conservation finance approaches, may be new or untested for certain audiences. Raising funds from conventional resources and then piloting new options over time may be the best approach to introduce novel income sources. For example:

- New finance options, such as environmental impact bonds, could be introduced over a longer period and trialed at a small scale, then scaled up when successful. These could also include other financial mechanisms, such as revolving loan funds (offering low-interest loans), public-private partnerships, or bonds.

- Other revenue-generating options could be tested in the same manner to ensure their effectiveness and introduce them to skeptical participants, financial managers, or government entities that are not used to working with alternative finance options.

Collaborative finance is a conservation finance strategy that involves cooperative interaction between individual project developers, stakeholders, and finance providers (Russell & Odefey, 2024). This process may or may not include traditional financial institutions. The term can be broadened to include finance developed through the fair and equitable participation of stakeholders in a region, landscape, or watershed, addressing natural resource and infrastructure management needs, and utilizing multiple forms of funding, from public grants to private investment. Finance approaches may include outcomes-based finance models such as environmental impact bonds.

The challenge of new finance options vs. more traditional approaches is, simply put, they’re new. As a result, more conservative controllers, accountants, and similar financial managers within any organization will be resistant to implementing new, unproven methods for generating income. Consequently, it may be best to start strong with traditional approaches and gradually test new strategies. Feasibility studies may also help introduce collaborative finance and new approaches. However, there are examples of established and successful impact finance bonds on the North Yuba River to draw upon when creating novel funding streams.

Funding JPAs is not a simple task, as most public funding sources are focused on project implementation, e.g., funding restoration projects in the field, rather than providing administrative support or organizational startup. Some foundations fund this type of work, but accessing those funds can be challenging. Another challenge is competing with existing entities for scarce local, regional, and federal resources. The following are recommendations to consider when examining the feasibility of building and maintaining a JPA for long-term feedstock agreements:

- Utilize public funds for startup and traditional projects. Public funding is readily available and generally suitable for trials or the initial development of feasible but new ideas.

- Pilot non-traditional, higher risk, or new revenue sources. Then, ramp them up with success, and participating entities and partners see their value and understand how they work.

- Co-house staff and resources. Utilize existing offices and share staff and other resources as capacity and funding allow. This is particularly important during the startup and early phases of developing a JPA.

- Leverage public funds with private investment. When public funds are secured, immediately work to leverage them with other public and private funding resources. Don’t wait until near the end of the grant cycle to look for additional funds.

- Use the right revenue source. Property and sales tax increases are more effective in populated areas with higher incomes; however, they are usually not appropriate for rural areas, where the tax base and population tend to be too low to provide sufficient funding.

Status

LCI Pilot Project teams are actively fundraising around their Entity Action Plans and working with state agency staff on promoting the development funding strategy options as summarized in this article.

Points of Contact

LCI program lead – Michael Maguire, LCI

Special thanks to Vance Russell, 3point.xyz